I will start with the blank worksheets and then below provide a study guide and tomorrow I will fill in the worksheets so you can compare your answers.

Worksheet

assignment #1

A Short-Run

Production Function and the Law of Diminishing Returns

Date Due:

Right Now

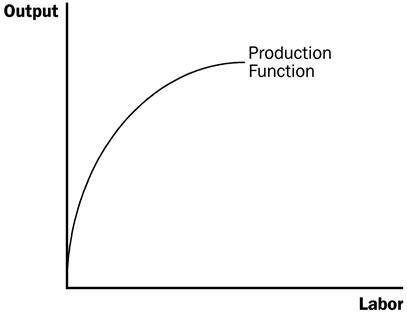

The production function shows the relationship (a

mathematical equation) between the amount of inputs and the amount of output

produced. Our focus will be on

the labor-output relationship for a

given level of capital and land.

N. P. Maplewood wishes to start a firm that

manufactures birdhouses. To

save on start-up costs, she will use the garden shed in her backyard as the

factory. Further, the shed has

a pile of lumber behind it and the shed is equipped with a saw, a drill, and

sandpaper.

She has all the

land and capital needed to

get started; she only needs to hire workers,

labor, to produce her product.

The data in the table below represents possible daily

output of birdhouses for various combinations of the variable output (labor)

with the two fixed resources (land and capital).

|

Units of the Variable Factor (Labor) |

Units of the Fixed Factor (Land & Capital) |

Total Product (TP) |

Marginal Product (MP) |

Average Product (AP) |

|

0 |

2 |

0 |

-- |

|

|

1 |

2 |

2 |

|

|

|

2 |

2 |

7 |

|

|

|

3 |

2 |

15 |

|

|

|

4 |

2 |

25 |

|

|

|

5 |

2 |

40 |

|

|

|

6 |

2 |

50 |

|

|

|

7 |

2 |

58 |

|

|

|

8 |

2 |

63 |

|

|

|

9 |

2 |

65 |

|

|

|

10 |

2 |

66 |

|

|

Complete the

table.

Base on the table on page 1, graph the short-run

production function, the relationship between output and labor, in the top

graph and both the marginal and average products of labor in the bottom

graph.

Production Function

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 2

3 4

5 6

7 8

9 10

Marginal

Product & Average Product

|

14 12 10

8

6

4

2 |

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

1 2

3 4

5 6

7 8

9 10

Answer the

following questions based on your table and graphs.

1.

State clearly and concisely the Law of Diminishing

Marginal Productivity.

2.

Does the marginal product of labor increase,

decrease, or not change for between 0 and 5 workers?

3.

Does the marginal product of labor increase,

decrease, or not change for more than 5 workers?

4.

How many units of labor will result in

maximum:

5.

Do technological improvements prevent or simply

cushion the effects of diminishing marginal productivity?

Why?

6.

How would an increase in technology affect the table

and your graphs?

Some

Notes on Production Theory

Short-Run – A

period of time in which there is at least one resource that is fixed and can not

be changed in the current production process.

Long Run – A

period of time sufficiently long so that producers are able to change the

quantities of all the resources they employ.

It is the “planning horizon” for the firm.

Variable Inputs

– Inputs that vary in quantity employed with the level of output.

Labor and raw materials are frequently raw materials.

Fixed Inputs –

Inputs that do not vary with the level of output in the short-run.

Salaries, insurance, and rent are some examples.

Production Function

or Total Product Function – shows the relationship between a firm’s inputs

or resources and the amount of output produced.

Law of Diminishing

Returns – As more and more of a variable resource is added to a production

process that has at least one fixed input, eventually the additional

output the firm gets from that variable input is going to fall.

Change In Total Product

Marginal Product

=

--------------------------------

Change in the Variable Input

Total Product

Average Product =

-------------------

![]() Variable

Input

Variable

Input

Worksheet assignment

#2

An Introduction to

Costs and Review of the Marginal Product

Date Due:

Right Now

Remember N. P. Maplewood and her birdhouse factory in the

shed out back. She has just come to

the realization that her friends will not work for free and her parents have

informed her that she must pay rent to use the shed, tools, and the lumber.

Producing goods involves costs.

We will explore her marginal product in relation to her marginal costs in

this worksheet.

N. P. must pay her friends $20 per day to build birdhouses

and she must pay her parents $100 for rent to be allowed to use the shed, the

tools, and wood pile in the back yard.

Fill in the blanks below.

|

Units of the Variable Factor (Labor) |

Total Product (TP) |

Marginal Product (MP) |

Fixed Costs (FC) |

Variable Costs (VC) |

Total Costs (TC) |

Marginal Costs (MC) |

|

0 |

0 |

-- |

|

|

|

-- |

|

1 |

2 |

|

|

|

|

|

|

2 |

7 |

|

|

|

|

|

|

3 |

|

8 |

|

|

|

|

|

4 |

25 |

|

|

|

|

|

|

5 |

|

15 |

|

|

|

|

|

6 |

50 |

|

|

|

|

|

|

7 |

|

8 |

|

|

|

|

|

8 |

63 |

|

|

|

|

|

|

9 |

|

2 |

|

|

|

|

|

10 |

66 |

|

|

|

|

|

Answer the following questions:

1.

The law of marginal productivity (law

of diminishing returns) begins with worker ___

2.

Define Marginal Costs in everyday language.

3.

Marginal costs first __________ and then __________.

This pattern occurs because marginal productivity (returns)

first _________ and then __________.

Worksheet assignment

#3

The Fixed Cost,

Variable Cost, and Total Cost Curves.

Date Due:

Right Now

N. P. Maplewood is still trying to understand the costs in

her birdhouse factory in the shed out back.

We will explore the shapes of her cost curves in this worksheet.

Remember that N. P. must pay her friends $20 per day to

build birdhouses and she must pay her parents $100 for rent to be allowed to use

the shed, the tools, and wood pile in the back yard.

Fill in the banks below.

|

Units of the Variable Factor (Labor) |

Total Product (TP) |

Fixed Costs (FC) |

Variable Costs (VC) |

Total Costs (TC) |

|

0 |

0 |

|

|

|

|

1 |

2 |

|

|

|

|

2 |

7 |

|

|

|

|

3 |

15 |

|

|

|

|

4 |

25 |

|

|

|

|

5 |

40 |

|

|

|

|

6 |

50 |

|

|

|

|

7 |

58 |

|

|

|

|

8 |

63 |

|

|

|

|

9 |

65 |

|

|

|

|

10 |

66 |

|

|

|

Use this information to complete the graphs and questions

on the follow pages.

Graph the Fixed Cost, Variable Cost, and Total Cost on the

graph below.

300 200 100

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5

10 15

20 25

30

35 40

45 50

55 60

65 70

1.

The fixed cost curve (increases, decreases, does not

change) ________________.

2.

The total cost curves starts by increasing at an

(increasing, decreasing) _________ rate and continues increase but at an

(increasing, decreasing) ____________ rate.

3.

What causes the pattern described in problem 2?

Worksheet assignment

4

The Average Cost

Curves and the Marginal Cost Curves

Date Due:

Right Now

N. P. Maplewood has just learned about average costs and

marginal costs and is trying to relate them to her birdhouse factory in the shed

out back. We will explore her

average costs in relation to her marginal costs in this worksheet.

Remember that N. P. must pay her friends $20 per day to

build birdhouses and she must pay her parents $100 in rent to be allowed to use

the shed, the tools, and wood pile in the back yard.

Fill in the banks below.

|

Units of the Variable Factor (Labor) |

Total Product (TP) |

Fixed Costs (FC) |

Variable Costs (VC) |

Total Costs (TC) |

Average Fixed Costs (AFC) |

Average Variable Costs (AVC) |

Average Total Costs ATC) |

Marginal Costs (MC) |

|

0 |

0 |

100 |

0 |

100 |

|

|

|

|

|

1 |

2 |

100 |

20 |

120 |

|

|

|

|

|

2 |

7 |

100 |

40 |

140 |

|

|

|

|

|

3 |

15 |

100 |

60 |

160 |

|

|

|

|

|

4 |

25 |

100 |

80 |

180 |

|

|

|

|

|

5 |

40 |

100 |

100 |

200 |

|

|

|

|

|

6 |

50 |

100 |

120 |

220 |

|

|

|

|

|

7 |

58 |

100 |

140 |

240 |

|

|

|

|

|

8 |

63 |

100 |

160 |

260 |

|

|

|

|

|

9 |

65 |

100 |

180 |

280 |

|

|

|

|

|

10 |

66 |

100 |

200 |

300 |

|

|

|

|

Use this information to complete the graphs and questions

on the follow page.

Marginal Cost on the graph below.

Notice the scale on the Y-axis.

Some of the values are too great to be included on the graph, but you can

estimate the shape of the curves after you have obtained some points on the

graph

20 10

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5

10 15

20 25

30

35 40

45 50

55 60

65 70

1.

Describe the shape of the average fixed cost.

2.

Describe the shape of the average variable cost and the

average total cost.

3.

Approximately where do the marginal cost and average

total cost curves cross.

4.

What is the relationship between the marginal cost curve

and the total cost curve.

When the marginal cost curve is (above, below) ___________

the average total cost, average total cost is (increasing, decreasing)

___________ and when the marginal

cost curve is (above, below) _________ the average total cost, average total

cost is (increasing, decreasing) ___________.

Worksheet assignment

#

Profit Maximization

Part II

Date Due:

Right Now

The assignment will be

graded out of a possible of XX points.

Just like before, her friends are $20 per day and she must

pay her parents $100 for rent to be allowed to use the shed, the tools, and wood

pile in the back yard. The improved

situation with the power tools is below.

The current price for birdhouses is $10.

Fill in the blanks below.

|

Units of the Variable Factor (Labor) |

Total Product (TP) |

Fixed Costs (FC) |

Variable Costs (VC) |

Total Costs (TC) |

Marginal Cost (MC) |

Marginal Revenue (MR) |

|

0 |

0 |

100 |

0 |

100 |

|

|

|

1 |

2 |

100 |

20 |

120 |

|

|

|

2 |

7 |

100 |

40 |

140 |

|

|

|

3 |

15 |

100 |

60 |

160 |

|

|

|

4 |

25 |

100 |

80 |

180 |

|

|

|

5 |

40 |

100 |

100 |

200 |

|

|

|

6 |

50 |

100 |

120 |

220 |

|

|

|

7 |

58 |

100 |

140 |

240 |

|

|

|

8 |

63 |

100 |

160 |

260 |

|

|

|

9 |

65 |

100 |

180 |

280 |

|

|

|

10 |

66 |

100 |

200 |

300 |

|

|

1.

Provide a mathematical definition for marginal cost.

2.

Define marginal costs in “everyday” language.

3.

Provide a mathematical definition for marginal revenue.

4. Define

marginal revenue in “everyday”

language.

5. At what

level of output is profit maximized?

I. What Are Costs?

A.

Total Revenue, Total Cost, and Profit

1.

The goal of a firm is to.......

3. Definition of total cost:.................

4.

Definition of profit:.................

B.

Costs as Opportunity Costs

1.

Principle #2: The cost of something is what you give up to get it.

Accountants focus on explicit costs, while economists examine both

explicit and implicit costs.

D.

Economic Profit versus Accounting Profit

Definition of economic profit:

Definition of accounting profit:

If implicit costs are greater than zero, accounting profit will always

exceed economic profit.

II.

Production and Costs

A.

The Production Function

1. Definition of production function: .........

|

Number of Workers |

Output |

Marginal Product of Labor |

Cost of Factory |

Cost of Workers |

Total Cost of Inputs |

|

0 |

0 |

--- |

$30 |

$0 |

$30 |

|

1 |

50 |

50 |

30 |

10 |

40 |

|

2 |

90 |

40 |

30 |

20 |

50 |

|

3 |

120 |

30 |

30 |

30 |

60 |

|

4 |

140 |

20 |

30 |

40 |

70 |

|

5 |

150 |

10 |

30 |

50 |

80 |

|

6 |

155 |

5 |

30 |

60 |

90 |

![]()

. Definition of marginal product:

Definition of diminishing

marginal product..........

We can draw a graph of the firm's production function by plotting the

level of labor (x-axis) against the

level of output (y-axis).

B.

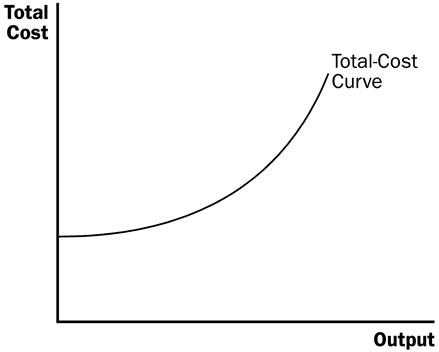

From the Production Function to the Total-Cost Curve

1.

We can draw a graph of the firm's total cost curve by plotting the level

of output (x-axis) against the total

cost of producing that output (y-axis).

a.

The total cost curve eventually gets steeper and steeper as output rises.

b. This increase in the slope of the total cost curve is also due to diminishing marginal product:

III. The Various Measures of Cost

1. Definition of fixed costs: ...............

2. Definition of variable costs:............

![]()

3. Total cost is equal to

fixed cost plus variable cost.

C.

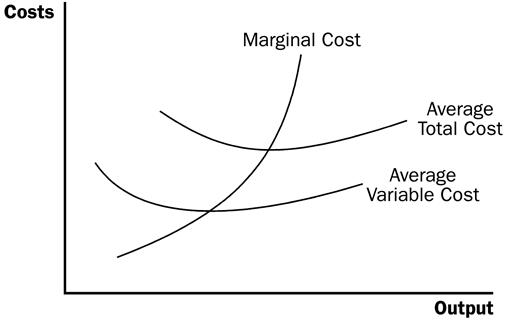

Average and Marginal Cost

1. Definition of average total cost: ...................

2. Definition of average fixed cost: ..................

3. Definition of average variable cost:.............

4.

Definition of marginal cost:

the increase in total cost that arises from an extra unit of production.

5.

Average total cost tells us the cost of a typical unit of output and

marginal cost tells us the cost of an additional unit of output.

D.

Cost Curves and Their Shapes

1.

Rising Marginal Cost

a.

This occurs because of diminishing marginal product.

b.

At a low level of output, there are few workers and a lot of idle

equipment. But as output increases, the coffee shop gets crowded and the cost of

producing another unit of output becomes high.

2.

U-Shaped Average Total Cost

a.

Average total cost is the sum of average fixed cost and average variable

cost.

b.

AFC declines as output expands

and AVC typically increases as output

expands. AFC is high when output

levels are low. As output expands, AFC

declines pulling ATC down. As fixed

costs get spread over a large number of units, the effect of

AFC on

ATC falls and

ATC begins to rise because of

diminishing marginal product.

3.

The Relationship between Marginal Cost and Average Total Cost

a.

Whenever marginal cost is less than average total cost, average total

cost is falling. Whenever marginal cost is greater than average total cost,

average total cost is rising.

b.

The marginal-cost curve crosses the average-total-cost curve at minimum

average total cost (the efficient scale).

4.

Typical Cost Curves

a.

Marginal cost eventually rises with output.

b.

The average-total-cost curve is U-shaped.

c.

Marginal cost crosses average total cost at the minimum of average total

cost.

I.

What Is a Competitive Market?

1. Definition of perfectly competitive market:

B.

The Revenue of a Competitive Firm

2.

Definition of average revenue:.......

3.

Definition of marginal revenue:....

II.

Profit Maximization and the Competitive Firm's Supply Curve

|

Q |

Total Revenue |

Total Cost |

Profit |

Marginal Revenue |

Marginal Cost |

Change in Profit |

|

0 |

$0 |

$3 |

$-3 |

---- |

---- |

---- |

|

1 |

6 |

5 |

1 |

$6 |

$2 |

$4 |

|

2 |

12 |

8 |

4 |

6 |

3 |

3 |

|

3 |

18 |

12 |

6 |

6 |

4 |

2 |

|

4 |

24 |

17 |

7 |

6 |

5 |

1 |

|

5 |

30 |

23 |

7 |

6 |

6 |

0 |

|

6 |

36 |

30 |

6 |

6 |

7 |

-1 |

|

7 |

42 |

38 |

4 |

6 |

8 |

-2 |

|

8 |

48 |

47 |

1 |

6 |

9 |

-3 |

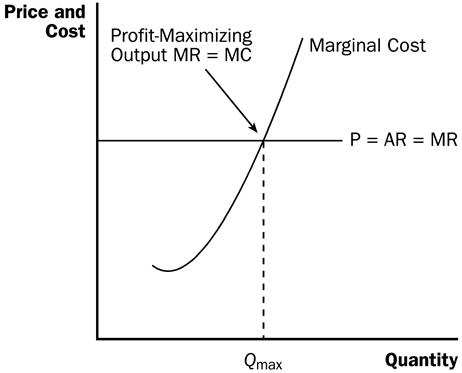

1.

In this example, profit is maximized if the farm produces four or five

gallons of milk (see the fourth column).

2.

The profit-maximizing quantity can also be found by comparing marginal

revenue and marginal cost.

a.

As long as marginal revenue exceeds marginal cost, increasing output will

raise profit.

b.

If marginal revenue is less than marginal cost, the firm can increase

profit by decreasing output.

c. Profit-maximization

occurs where marginal revenue is equal to marginal cost.

1.

Cost curves have special features that are important for our analysis.

a.

The marginal-cost curve is upward sloping.

b.

The average-total-cost curve is U-shaped.

c.

The marginal-cost curve crosses the average-total-cost curve at the

minimum of average total cost.

2.

Marginal and average revenue can be shown by a horizontal line at the

market price.

3.

To find the profit-maximizing level of output, we can follow the same

rules that we discussed above.

a.

If marginal revenue is greater than the marginal cost, the firm should

increase its output.

b.

If marginal cost is greater than marginal revenue, the firm should

decrease its output.

c.

At the profit-maximizing level of output, marginal revenue and marginal

cost are exactly equal.