I.

Markets and Competition

A. What Is a

Market?

1. Definition of market:

B. What Is

Competition?

1. Definition of competitive market:

C. In this

chapter, we will assume that markets are perfectly competitive.

1.

Characteristics of a perfectly competitive market:

a. The goods

being offered for sale are exactly the same.

b. The buyers

and sellers are so numerous that no single buyer or seller has any influence

over the market price.

2. Because

buyers and sellers must accept the market price as given, they are often called

"price takers."

3. Not all

goods are sold in a perfectly competitive market.

a. A market

with only one seller is called a monopoly market.

b. Other

markets fall between perfect competition and monopoly.

II. Demand

A. The Demand

Curve: The Relationship between Price and Quantity Demanded

1. Definition of quantity demanded:

Definition of law of demand:

Definition of

demand schedule:

|

Price of Ice Cream Cone |

Quantity of Cones Demanded |

|

|

$0.00 |

12 |

|

|

$0.50 |

10 |

|

|

$1.00 |

8 |

|

|

$1.50 |

6 |

|

|

$2.00 |

4 |

|

|

$2.50 |

2 |

|

|

$3.00 |

0 |

|

4. Definition

of demand curve:

a. Price is

drawn on the vertical axis.

b. Quantity

demanded is represented on the horizontal axis.

Shifts in the

Demand Curve

If any of these other factors change, the demand curve will

shift.

a. An increase

in demand is represented by a shift of the demand curve to the right.

b. A decrease

in demand is represented by a shift of the demand curve to the left.

Income

a. The

relationship between income and quantity demanded depends on what type of good

the product is.

b. Definition

of normal good: a good for which,

other things equal, an increase in income leads to an increase in demand.

c. Definition of inferior good: a good for which, other things equal, an increase in income leads to a decrease in demand.

Prices of Related

Goods

a. Definition

of substitutes: two goods for

which an increase in the price of one good leads to an increase in the demand

for the other.

b. Definition

of complements: two goods for

which an increase in the price of one good leads to a decrease in the demand for

the other.

Tastes

Expectations

a. Future

income

b. Future

prices

7. Number of Buyers

III. Supply

A.

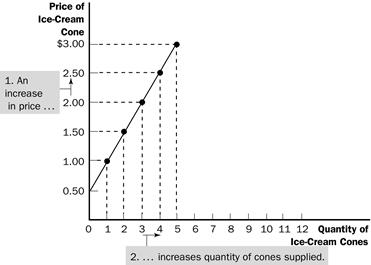

The Supply Curve: The Relationship between Price and Quantity Supplied

1. Definition

of quantity supplied:

a. Quantity

supplied is positively related to price. This implies that the supply curve will

be upward sloping.

b. Definition of law of supply:

2. Definition of supply schedule:

3. Definition

of supply curve:

|

Price of Ice Cream Cone |

Quantity of Cones Supplied |

|

$0.00 |

0 |

|

$0.50 |

0 |

|

$1.00 |

1 |

|

$1.50 |

2 |

|

$2.00 |

3 |

|

$2.50 |

4 |

|

$3.00 |

5 |

2. Input Prices

3. Technology

4. Expectations

5. Number of

Sellers

IV. Supply and Demand

Together

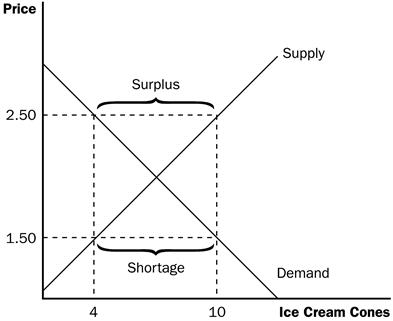

A. Equilibrium

1. The point

where the supply and demand curves intersect is called the market’s equilibrium.

2. Definition of equilibrium:

3. Definition of equilibrium price:

4. The

equilibrium price is often called the "market-clearing" price because both

buyers and sellers are satisfied at this price.

5. Definition

of equilibrium quantity: the

quantity supplied and the quantity demanded at the equilibrium price.

6. If the

actual market price is higher than the equilibrium price, there will be a

surplus of the good.

a. Definition

of surplus:

b. To

eliminate the surplus, producers will lower the price until the market reaches

equilibrium.

7. If the

actual price is lower than the equilibrium price, there will be a shortage of

the good.

a. Definition of shortage:

b. Sellers

will respond to the shortage by raising the price of the good until the market

reaches equilibrium.

B. Three Steps

to Analyzing Changes in Equilibrium

1. Decide

whether the event shifts the supply or demand curve (or perhaps both).

2. Determine

the direction in which the curve shifts.

3. Use the

supply-and-demand diagram to see how the shift changes the equilibrium price and

quantity.